A number of customers of Nuran Bank complained about another disruption affecting the bank’s application, preventing them from carrying out financial transfers through the banking app.

This comes despite the bank’s repeated promotional campaigns, amid growing frustration among customers over the recurring outages and technical issues.

Written by: Dr. Ayoub Mohamed Al-Farsi, member of the Central Bank’s Monetary Policy Committee

The availability of cash US dollars and the ease of obtaining them through official channels is a true indicator of the recovery of the banking sector. During economic crises, foreign currency shifts from being merely a medium of exchange to a store of value and a symbol of stability.

Impact of Receiving Cash Dollars on Restoring Trust The ability of a depositor to withdraw their savings or allocations in US dollars “in cash,” as well as the ability of traders to transfer payments for goods through official channels, represents the ultimate test of banking credibility.

Breaking the fear barrier: When citizens are reassured that their money is not just “numbers on paper” and can be liquidated at any time, they stop rushing to withdraw deposits. This is further reinforced by the significant progress made by the Central Bank in digital transformation.

Reviving banking circulation: Restored confidence means the return of savings from “homes” to “bank vaults,” even partially, increasing bank liquidity and their ability to finance projects.

Unified spending agreement and government centralization Fiscal and monetary policy are two sides of the same coin. A unified spending framework eliminates chaos in public expenditure—what if it is accompanied by a unified government?

Controlling the deficit: Unifying spending channels prevents duplication and waste of resources, reducing pressure on foreign reserves.

Attractive investment environment: Investors, both local and foreign, require a clear and unified fiscal vision to assess risk—something only achievable by ending financial fragmentation.

Reducing the gap between official and parallel exchange rates When the official exchange rate approaches the parallel market rate, demand behavior changes:

Decline in speculation: When the gap is wide, demand for dollars is driven by profit-seeking. When rates converge, demand becomes limited to real needs such as trade, travel, or medical treatment.

Consumption rationalization: Real demand stabilizes the exchange rate and prevents wasteful depletion of foreign currency.

Role of dollar sales in controlling money supply Selling US dollars by the Central Bank is a powerful monetary policy tool to absorb excess liquidity:

Liquidity absorption: When the Central Bank sells dollars, it withdraws local currency from circulation, reducing money supply (M2).

Inflation control: A reduced money supply lowers excessive purchasing power chasing goods, helping reduce inflation and stabilize prices.

Finally, restoring trust is not merely an administrative decision, but the natural outcome of realistic monetary policies, unified political and financial decision-making, and ensuring foreign currency flows to those who deserve it at a fair exchange rate.

The General Manager of the Libyan Islamic Bank, Adel Kashad, told our source that the letter imposing a travel ban on him was issued by an entity lacking legal legitimacy. He noted that this was confirmed by the Office of the Public Prosecutor in its correspondence to public authorities, emphasizing that investigative procedures must be handled exclusively by the legitimate authority—not the entity that imposed the travel ban.

He stated that, legally, a travel ban can only be issued by the judiciary or the Public Prosecutor, and no other body has the authority to enforce such a decision.

Kashad added that he had previously facilitated cooperation by allowing the concerned party to establish an office within the bank. However, they later submitted unlawful requests, including demands to disclose confidential bank account information in violation of the law.

He further stressed that all banking operations at the Libyan Islamic Bank are conducted in accordance with applicable legislation and are subject to oversight by the Central Bank of Libya. He affirmed that these measures are a legal obligation to protect banking confidentiality and safeguard customer data.

Our source has obtained leaks from a meeting of the Central Bank’s Board of Directors indicating that foreign currency will be sold to exchange companies according to the funds available in their accounts, or up to 70% of the balance in the exchange company’s or exchange office’s account at the Commercial Bank.

This will be done without a specified cap on the volume of currency.

Our banking source told in an exclusive statement that the U.S. dollar is expected to fall below 8 dinars in the parallel market, as a result of anticipated measures by the Central Bank of Libya and the Ministry of Economy, along with the activation of exchange companies and their provision with foreign currency by the Central Bank.

The source said this will take place in accordance with the agreed mechanism, pending the announcement of the Central Bank’s procedures tomorrow or next Sunday, and the reopening of foreign currency platforms.

Written by legal advisor Mustafa Al-Manea: Lebanon’s new law on deposit recovery is “a complex surgery after the disease has worsened,” published on Arabi 21 link.

The financial and banking crisis that erupted in Lebanon in 2019 represents one of the deepest monetary and financial crises in the modern history of developing countries—not only in terms of the scale of losses but also in the way it was managed and the delay in acknowledging it. With the Lebanese government recently approving the draft law to address the financial gap and recover deposits, discussions have centered on the state’s role in protecting the monetary system.

The Lebanese pound has lost more than 90% of its value against the dollar since 2019. From about 1,500 Lebanese pounds per U.S. dollar, the pound rapidly collapsed to between 85,000 and 100,000 pounds per dollar.

Photo of Advisor Al-Manea from the official U.S. Federal Reserve headquarters.

First: Roots of the Crisis – When the Banking System Becomes a Tool for Financing Public Debt

The Lebanese crisis was not the result of a sudden external shock but the outcome of chronic structural imbalances, most notably:

Intertwining of Public Finance and the Banking Sector Commercial banks became the main financiers of public debt, concentrating sovereign risks within the banking system.

Unsustainable Monetary Policies The Central Bank of Lebanon relied on complex financial instruments to maintain exchange rate stability, effectively using people’s deposits to temporarily support this stability instead of directing them toward investment in production and the real economy.

Lack of Transparency and Accountability The true scale of losses was not disclosed early, and recognition of the so-called financial gap was delayed, allowing depositors’ rights to erode cumulatively. Bank assets fell from about $217 billion in 2019 to around $104 billion by 2024, while customer deposits shrank from roughly $172 billion to about $88 billion in the same period.

Second: The Deposit Recovery Law Represents a Delayed but Necessary Remedy

The draft law to address the financial gap and recover deposits attempts to provide a legal framework for what was previously managed through norms and unofficial restrictions.

Key economic features of the law include:

Official recognition of losses and determination of responsible parties (state, central bank, banks).

Relative protection for small and medium depositors by refunding deposits up to a certain limit within a set timeframe.

Conversion of part of large deposits into long-term financial instruments, effectively restructuring deposits.

Introduction of the concept of loss-sharing (Burden Sharing) instead of placing it on a single party.

According to government statements, 85% of depositors may recover their full deposits within four years under this law.

Third: Challenges and Limits of the Law

Despite its importance, the law faces several fundamental issues:

Lack of Clear Funding Sources Refunding deposits without specifying real foreign currency sources makes implementation dependent on economic growth or the sale of public assets.

Prolonging the Crisis Long-term repayment may turn immediate losses into a chronic burden, constraining investment and growth for years.

Limited Accountability Without clear accountability for banking management and monetary decision-makers, moral hazards remain, and risks to reputation and trust are expected.

Amid the ongoing crisis, indicators—though needing verification—suggest that nearly half of deposits have eroded or lost their real value since 2019 due to currency collapse and unregulated revaluation processes.

Fourth: Lessons Learned – What Should Not Be Repeated

No Monetary Stability Without Fiscal Discipline Lebanon’s experience shows that stabilizing the exchange rate or protecting the currency cannot be achieved by banks alone; it requires disciplined public finance and genuine tax reform.

Lebanon’s GDP has contracted by more than 40% since 2019, reflecting the profound impact beyond the banking sector, affecting the real economy. The issue becomes even more complex when banks are partly responsible for creating distortions and instability in public finance.

Deposit Protection is Not Just a Slogan but a System The absence of an effective deposit insurance system and weak banking governance made depositors the weakest link. A sound banking system requires:

Strict risk management rules

True separation between banks and the state

Immediate transparency in financial statements

Delaying Loss Recognition Multiplies Them The most dangerous aspect of Lebanon’s experience is not the size of losses but the postponement of acknowledging them, which enabled capital flight, deposit erosion, and collapse of trust.

Legislation Cannot Succeed Without Comprehensive Reform Deposit recovery laws cannot succeed in isolation from:

Reform of the Central Bank of Lebanon

Restructuring of banks

Stimulating the real economy (production, export, investment)

Conclusion

Lebanon’s experience should serve as an early warning for any similar practices.

The recent Lebanese law is a delayed but necessary step toward resolving the crisis. However, it reminds us that crisis management is measured not only by legal texts but by their timing, transparency, fairness, and performance indicators.

The Lebanese experience includes financial losses estimated in tens of billions of dollars and a dramatic decline in the local currency’s purchasing power, severely affecting depositors’ ability to maintain their wealth.

When banks become a tool for financing public spending and reform is replaced by postponement, depositors’ funds become the fuel of the crisis, not just its victims.

These are critical lessons for any country seeking to protect its currency, depositors, and economic stability before it’s too late. Lebanon’s new law represents a necessary and complex “surgery” after the disease has worsened.

Author: Legal Advisor Mustafa Al-Manea, a Libyan lawyer and legal-economic expert with over 24 years of experience. He has worked with investment institutions, sovereign funds, and banks worldwide, including Libya. He is an expert for international research centers, has served as an advisor to the Governor of the Central Bank of Libya, chaired several executive teams, sits on the board of the Libyan Investment Authority and the Libyan Foreign Bank, represented Libya at World Bank and IMF meetings, and leads the Prime Minister’s executive initiatives and strategic projects. He has lectured for the American Bar Association, is a certified member of the European Lawyers Association, a member of the Libyan-American Business Council, and has numerous publications and bold opinions on economic and financial transformation.

Our has obtained a copy of a decision issued by the Central Bank of Libya, in which it addressed banks as well as licensed exchange offices and companies, inviting them to a meeting next Thursday, January 1, 2026.

The meeting aims to regulate the work of licensed companies and offices so that they can perform their role in accordance with the law, in support of the national economy and with the provision of all necessary support to them.

The Trade and Development Bank exclusively revealed to Sada Economic Newspaper that it has postponed the implementation of its circular, which contradicts the instructions of the Central Bank of Libya and is attributed to the Control Department branch at the Central Bank in Benghazi.

This circular concerns requiring the deposit of the value of foreign currency card top-ups in cash instead of electronic payment, and its implementation has been deferred until the beginning of 2026.

Our source has exclusively obtained a circular issued by the Trade and Development Bank to its branches, requiring that the value of foreign currency card recharges be deposited in cash instead of using electronic payment methods.

This step runs counter to the directions of the Central Bank of Libya, which call for the adoption of electronic payment instruments. Specialists consider that this measure could contribute to widening the exchange rate gap applied by the bank.

Written by consultant Mustafa Al-Manea, Libya and the African Development Bank Strategy 2025–2028

At this stage, Libya seeks to move beyond traditional models of financing development projects and to abandon exclusive reliance on the public budget. This comes as the Government of National Unity works to restore confidence with regional and international partners, stimulate foreign capital, and leverage external financing instruments. In this context, the renewed partnership with the African Development Bank (AfDB) stands out as one of the most important practical tools to support this transformation, especially after the Bank adopted this week a Strategic Cooperation Framework with Libya for the period 2025–2028.

The Bank, which counts more than 80 African and non-African countries among its members and manages an annual financing portfolio exceeding USD 10 billion, does not limit its role to providing loans. Rather, it supports governance, institution-building, and the mobilization of financing from multiple sources. This approach is of particular importance for Libya, which today is searching for sustainable financing and development solutions.

The launch of the Bank’s 2025–2028 strategy coincides with the Government of National Unity, headed by Abdul Hamid Dbeibeh, adopting a more open approach toward economic reform, stimulating development, and building partnerships with foreign investors.

However, the structural challenge within the public spending framework remains. Salaries and subsidies consume more than 70% of the general budget, leaving only a limited margin for development and investment. This makes reliance on public resources alone insufficient to drive economic growth or create sustainable employment opportunities.

Key Pillars of the Strategy

The Bank’s strategy for Libya for 2025–2028 focuses on several key objectives, most notably:

Strengthening governance and public financial management, including support for budget reforms, improving spending efficiency, and developing transparency and accountability systems, including the digital transformation of public finance.

Rehabilitating and developing infrastructure, particularly in the electricity, water, transport, and logistics sectors, to ensure an environment attractive to private investment.

Focusing on the energy sector and energy transition, supporting the sustainability of the electricity grid, improving energy efficiency, and preparing Libya to gradually benefit from renewable energy projects.

Agriculture and food security, by modernizing agricultural value chains, developing irrigation systems, and linking local production to markets, thereby reducing dependence on imports.

Empowering the private sector and small and medium-sized enterprises, by improving access to finance, enhancing the business environment, and supporting entrepreneurship, especially among youth.

Previous Experiences of the Bank

The African Development Bank’s experience has proven successful in countries such as Morocco, Egypt, Kenya, Ethiopia, Senegal, and Rwanda, where the Bank linked financing interventions to institutional reforms. In these and other countries, the Bank financed projects with direct economic and social impact, including electricity generation, transmission, and distribution projects; highways and cross-city and cross-border logistics corridors; water and sanitation plants; integrated agricultural programs (production, storage, transport, and marketing); credit lines for local banks to support the private sector; and public-private partnership (PPP) projects. These are models that can be adapted to the Libyan context.

Financing Instruments Available from the Bank

Among the financing tools that Libya can leverage from the Bank are:

Sovereign and non-sovereign guarantees to reduce investor risk

Co-financing with international institutions and sovereign wealth funds

Financing for public-private partnerships (PPP)

Direct financing for the private sector

Intra-African trade support windows

Conclusion

The African Development Bank’s strategy for the period 2025–2028, if coupled with the continued governance and reform efforts led by the Government of National Unity, can represent an opportunity to contribute to sustainable growth whose impact is felt by citizens and from which the state benefits over the long term.

Consultant Mustafa Al-Manea is a Libyan lawyer and legal and economic expert with more than 24 years of experience. He has worked with a number of investment institutions, sovereign funds, and banks in several countries around the world, including Libya. He serves as an expert for international research centers and worked for years as an advisor to the Central Bank of Libya. He has also served as a board member of the Libyan Investment Authority and the Libyan Foreign Bank, represented Libya in meetings of the World Bank and the International Monetary Fund, and heads the executive team for the Prime Minister’s initiatives and strategic projects. He has worked as an expert and lecturer with the American Bar Association and is a member of the Libyan-American Council for Trade and Investment. He has published numerous research papers and articles in Arab, American, and European newspapers and is known for his bold views on economic and financial transformation issues.

One of the residents of the Savings and Real Estate Investment Bank building in the Meizran area toldour source: “The apartments were previously rented to private companies. After these companies left in 2011, the apartments became empty. We moved in during 2013, and some of us at the end of 2012, with ownership certificates.”

He added: “When we entered the apartments, they had no windows, no doors, no elevator, and no water. We — 28 families — fixed everything ourselves. We installed doors and windows, repaired the water networks, and legally connected electricity through official meters.”

He continued: “We contacted the Savings Bank to sign housing contracts, but they told us at that time that the bank was closed, there were no new contracts, and that they were tied to the Land Registry and could not issue contracts for us.”

He also said: “In 2014, the General Manager of the Savings Bank, Jum’a Al-Nayed, came to the building, toured the entrances, and was very impressed by the changes we made. The building used to be like a den where young people gathered; it was in terrible condition. That all changed because of our efforts. But after that visit, nothing happened and no one followed up with us.”

He went on: “When we later tried again to contact the bank to sign contracts, the bank clearly refused. The branch we belonged to didn’t even have a manager. Whenever we asked, they said: ‘There is no manager yet, no one has been appointed. Please wait.’”

He added: “Recently, we received summonses from the Central Police Station. We complied and went to the prosecution, which issued arrest warrants. We remained detained for 18 days. They kept telling us: ‘Hand over the apartments you’re in and then leave,’ meaning they extorted us by depriving us of our freedom. This is a great injustice. We are Libyan families — 28 apartments, all inhabited by widows, divorced women, and poor families who cannot afford rent. Rental prices today are beyond people’s means; those who rent can barely eat or drink. We also have children.”

He continued: “They cut off the water supply from the beginning of October until now. People in the building have no water. Women over 60 years old climb high floors — the 5th, 6th, and 7th — carrying water in plastic containers. Only God knows their condition. The situation is truly tragic.”

He concluded: “We are Libyan citizens with civil rights, one of which is the provision of housing by the State.”

Our exclusive sources revealed that there are reports about the resignation of the General Manager of the National Commercial Bank, Ali Al-Khuwaildi, from his position.

According to the sources, the Deputy General Manager has been assigned to take over the role.

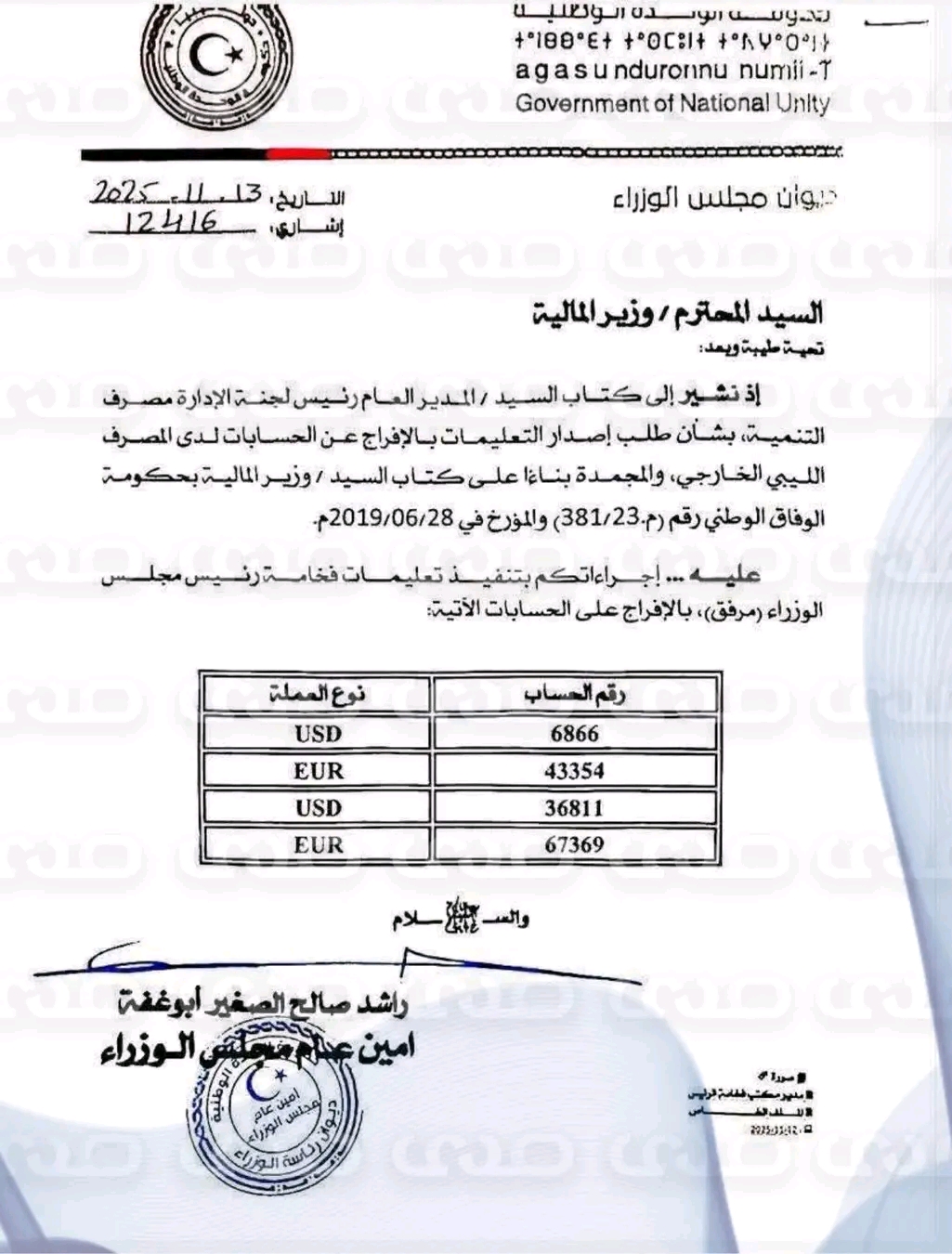

Our source has exclusively obtained a letter from the Secretary-General of the Council of Ministers of the Government of National Unity to the Minister of Finance regarding the correspondence of the Chairman of the Management Committee of the Development Bank, which included a request to release the accounts frozen at the Libyan Foreign Bank based on a previous order from the former Minister of Finance of the Government of National Accord.

The correspondence included instructions from Abdulhamid Dbeibeh to release the Development Bank’s accounts in dollars and euros.

The Governor of the Central Bank of Libya, Naji Issa, stated regarding the Banking Investment Initiative that it is not necessarily meant to be implemented next month, but rather to be ready as part of a broader vision. He emphasized that without a comprehensive economic vision aligning all policies and defining real objectives, such a project cannot achieve its goals. “The Central Bank’s initiative is one we are ready for today — a prepared document and project — but without restructuring and reforming Libya’s economy, no initiative will achieve its purpose. The Central Bank cannot operate independently in all areas, even in monetary policy,” he said.

Issa added: “Without the oil sector, we have no economy. We have initiatives, and the private sector is striving, but it faces many challenges. If oil prices drop to $52 per barrel, the state won’t be able to pay salaries. We must ask: What will Libya’s economy look like in the next three years? Will the state continue employing more than 2.5 million people in the public sector and spending 80 billion on salaries at the expense of development funding?”

He further noted that while government development projects have added value, they are not productive value-added projects and thus cannot be financed by the Holding Company. The credit extended by banks — often seen as consumer loans — actually covers citizens’ income deficits, since incomes have remained low for decades. “If we do not increase citizens’ purchasing power, private sector investments will not find the demand needed to consume the goods and services produced. Stimulating credit and purchasing power is what drives growth itself,” Issa explained.

He continued: “The banking sector is fulfilling its role, though there are shortcomings — not due to the Central Bank, but because of the circumstances we face. The situation and environment are not ideal for designing monetary or economic policies.”

Issa also pointed out that he is working with two governments — not by choice, but as a reflection of reality on the ground. “The Ministry of Economy is divided, the Ministry of Finance is divided, and so are all state institutions. How can we establish a Holding Company and launch it next month amid this division? Even political division has imposed a reality on the Central Bank. Everyone blames the banking sector and the Central Bank, but there are no magical solutions without a unified vision and functioning state institutions,” he said.

He revealed that the state currently needs around $3 billion based on current spending rates, while net revenues deposited in the Central Bank may not exceed $1.5 billion, posing a major fiscal challenge.

Issa concluded: “We have demands from traders, the private sector, and banks. We all hope that problems will be solved and citizens can live in prosperity — this is our goal and the government’s goal — but the current reality limits these solutions. The banking sector and the Central Bank are under pressure, yet hope remains in the initiatives that will soon be implemented.”

Assaray Trade and Investment Bank has recorded notable growth and outstanding financial results throughout its journey. The Chairman of the Board, Dr. Ahmed Atiga, and the General Manager, Farouk Al-Obaidi, presented the bank’s overall performance indicators, which reflected significant growth across various banking and investment activities. These include increases in assets, financing, deposits, and customer base, resulting in a net profit of 26% of the share’s nominal value, or about 9% return on equity, estimated at 325 million dinars, excluding the revaluation of fixed assets and goodwill.

The market price evaluation of ATIB’s shares, conducted by the international consulting firm KPMG, showed that the average fair value per share was estimated at 93 dinars, with an upper limit of 110.4 dinars and a lower limit of 76 dinars. This reflects the confidence of financial institutions in the bank’s performance and the sustainability of its growth.

Founded in 2005, ATIB is one of the leading institutions that have contributed to the development of modern and electronic banking services, enhancing the local investment environment.

Among the general assembly’s recommendations was the “unlimited support from shareholders to adopt technology and embrace continuous innovation, making ATIB a technologically advanced institution par excellence.”