Economic expert Omran Al-Shaeibi an article saying: Social media platforms have circulated the letter sent by the Central Bank to the Audit Bureau based on the warning issued by the U.S. Federal Reserve to the Central Bank regarding subjecting its dollar-denominated transactions to review and auditing.

This notice signals a serious risk in the nature of the relationship between the Libyan banking sector and international financial institutions and requires dealing with it with utmost seriousness. This measure falls under the “de-risking” policy described by the Financial Action Task Force (FATF), where financial institutions terminate or restrict commercial relationships with clients or categories of clients to avoid risks instead of managing them, in line with FATF’s risk-based approach.

What is the significance of this measure and its implications?

Firstly, the loss of institutional trust, as this procedure expresses deep doubts from the Federal Reserve about the Central Bank of Libya’s ability to manage its financial operations in accordance with international standards, affecting the reputation of the Central Bank and consequently reducing international transactions.

Secondly, complicating international financial operations and subjecting them to rigorous reviews or involving a third party in auditing processes, as noted in the letter, which could lead to disruptions in critical financial operations such as collecting oil revenues or facilitating essential imports.

Thirdly, direct economic repercussions due to restrictions on dollar-denominated transactions that could result in delays in fulfilling the state’s external obligations, negatively affecting national economic stability and impacting the state’s ability to provide essential goods or maintain monetary stability.

The application of the “de-risking” policy by international financial institutions, according to the FATF, is not only related to risks of money laundering and terrorism financing but also reflects a comprehensive view of the concerned institution and its adherence to the forty international standards set by the FATF. This does not require formal justification, as it pertains to risk management based on internal evaluations.

The Central Bank must improve its procedures and prove its ability to adhere to international standards to regain the trust of correspondent institutions, prevent delays in international financial transactions, avoid disruptions in financial flows with the outside world, enhance anti-money laundering and terrorism financing measures, develop a robust system for implementing “Know Your Customer” procedures, raise transparency levels in managing financial operations, involve reputable and trusted financial institutions as third parties to manage risks, seek advisory support from international financial institutions to improve compliance standards, and work on a long-term strategy.

When the Central Bank was stormed in the past period through uncalculated methods, it prompted international institutions to take measures that will remain strict until confidence in the financial institutions of the Libyan state is renewed.

We also trust the new board of directors and the technical staff at the bank to overcome this obstacle successfully.

The Central Bank of Libya exclusively revealed toour source that a new shipment of cash arrived this evening from abroad. The cash was immediately transported to the Central Bank’s vaults to prepare it for distribution to all branches of commercial banks in Libya, in accordance with the previously approved timeline.

This step comes as part of the Central Bank of Libya’s plan to ensure cash availability, under the directives of Mr. Naji Mohammed Issa, the Governor of the Central Bank, and his deputy.

Economic expert Mohammed Abu Snina wrote about the warning issued to the Central Bank by the U.S. Federal Reserve regarding the review and audit of its dollar-denominated transactions:

This measure falls under what is known as D-Risking, a procedure adopted by international financial institutions when they perceive financial risks associated with their transactions with certain banks or financial institutions. This often leads to suspending transactions with them.

Typically, the risks necessitating the review of financial transactions of a central bank or a financial institution operating in international markets include money laundering and terrorist financing risks (AML-CTF), as well as weak “Know Your Customer” (KYC) procedures applied by financial institutions under scrutiny for financial risks.

The measure reflects doubts about the financial institution’s ability to manage its funds transparently, implying a loss of trust in its management. This loss of trust is the worst scenario any financial institution can face.

The Federal Reserve’s decision to request the involvement of a third party to review financial operations with the Central Bank indicates that the Federal Reserve faces challenges in managing risks associated with financial transactions with the Central Bank and the Libyan banking sector in general or in managing these risks efficiently.

Naturally, the procedures adopted by international financial institutions to hedge against financial risks resulting from their dealings with various institutions vary from one institution to another, depending on the level of expected financial risks.

To continue financial transactions with high-risk institutions, third-party financial institutions with robust risk management systems are often engaged. These institutions are chosen based on their reputation and the financial risk management system they adopt.

According to the Financial Action Task Force (FATF), the application of D-Risking to any institution indicates a complex situation that goes beyond merely complying with anti-money laundering and terrorist financing procedures. It requires adherence to the full forty recommendations and standards of FATF directed at financial institutions. Notably, institutions implementing D-Risking policies with their clients are not obligated to justify the procedure or base it on judicial rulings. Risk management is an internal matter determined by the financial institution itself. The institution subjected to this procedure or ban (the customer or client) is only required to comply and rectify its situation.

Underestimating or downplaying the significance and seriousness of subjecting the Central Bank to D-Risking risks does not serve the national economy or the future of the Libyan banking and financial sector. This issue should be taken seriously and requires a strategy to ensure the sustainability of financial transactions with the external world. Such a strategy is necessary to avoid delays and disruptions to dollar-denominated transactions with correspondent banks abroad, including the collection of oil revenues in dollars. These disruptions would affect economic stability, the supply of consumer goods, the state’s ability to meet its external obligations, and result in losses for the Central Bank and the Libyan banking sector as a whole.

Financial expert Khaled Al-Zantouti exclusively told our source regarding the Central Bank’s recent statement: “The average Libyan household consumes imported goods and services worth over 21,000 Libyan dinars monthly, which is three times the value of our oil exports.”

He added, “I was deeply astonished by the Central Bank’s recent statement and the figures it disclosed. It stated that during just 18 days of December, $3.5 billion worth of currency purchase requests were processed. Of this, $1.7 billion was for letters of credit and another $1.7 billion for personal transfers—staggering figures.”

Al-Zantouti explained, “This means we are transferring approximately $200 million daily, equating to about one billion dinars per day, to fund imports and other purposes. And as for ‘other purposes,’ you can underline that ten times. One billion dinars daily—day after day—are spent by Libyans on food, drink, medical treatment, and other needs, all sourced in foreign currency and from outside Libya. This averages 143 dinars per individual per day, assuming a population of 7 million Libyans.”

He elaborated, “For a family of five, this translates to approximately 21,450 dinars in imported goods and services per month. (This assumes that the consumption by foreigners is ultimately borne by Libyans.) Is this reasonable?”

He added, “Now let’s take another perspective: Based on the average Brent crude price of $72.5 per barrel for the first 18 days of this month and factoring in daily export volumes, the foreign partner’s share, and local refinery consumption, Libya’s oil revenues will not exceed $1 billion over these 18 days. This means that even if the full value of these exports were deposited in the Central Bank’s external account, we would still face a hard currency deficit of over $2.5 billion. In essence, our consumption exceeds three times the value of our oil exports.”

He noted, “This analysis is solely for imported goods and services. It does not even account for salaries and other public budget expenditures. Whatever the reasons or justifications, even if tied to year-end processes or annual closures, these figures are alarming, frightening, and disheartening.”

He concluded with a wry remark: “And then they ask me, ‘Why are you pessimistic, Mr. Khaled?’”

Former Central Bank of Libya board member, Mrajaa Ghaith, commented to our source regarding the letter sent by the Central Bank to the Audit Bureau. He stated that these issues had been repeatedly highlighted in the past, referencing the Global Witness report that revealed corruption in letters of credit. He also warned about the risks associated with the “Family Heads Grant,” emphasizing that it should have been disbursed in Libyan dinars. Allowing citizens to sell dollars without controls over how the currency is used or identifying the real buyers posed significant risks.

The international audit report highlighted its inability to access the letters of credit system, further indicating a lack of control over the use of foreign currency. The government’s cancellation of its agreement with a company monitoring letters of credit raised suspicions about its capability to combat money laundering and terrorism financing. The international working group initiated a review process months ago, expressed concerns, but the matter was not taken seriously.

Ghaith added: “The way the letter was leaked, which is unethical, has raised doubts about the Central Bank’s continued ability to process and approve dollar transactions through the U.S. Federal Reserve system. Perhaps some are unaware that all dollar transactions pass through specific systems in the United States, with a focus typically on countries experiencing instability. The political factor in this field cannot be overlooked.”

The Head of the Accounting Department at the Libyan Academy, Abubakr Abu Al-Qasim, commented to our source on the open letter issued by several individuals concerned with financial matters. The meeting, organized by the Humanitarian Dialogue Center, led to the creation of a document that focused on returning to the legal foundations for approving the 2025 budget. The document also addressed short-term measures and tackled some of the distortions in financial policies adopted, particularly in recent years, rather than offering long-term strategies.

He added that the document did not address broader economic issues and instead focused on setting mechanisms for rationalizing government spending and enhancing revenues. It also highlighted legal violations related to spending, revenues, and the irresponsible use of public funds. The discussions were constructive, involving Libyan experts with knowledge and experience in this field, and should be considered in the context in which they were presented.

He also noted that this open letter was directed to all stakeholders involved in Libyan affairs, both domestic and international, at a critical time, especially as the country is actively working to reshape the Libyan landscape.

The World Bank reported today, Wednesday, that Libya’s economy is expected to stabilize following an agreement to resolve the country’s Central Bank crisis, which led to a significant rebound in oil production. However, despite recent progress, Libya’s GDP is expected to shrink by 2.7% by the end of 2024.

According to the latest World Bank report on Libya’s economy, economic expectations remain dependent on sustained political stability and strategic efforts to diversify the economy beyond hydrocarbons.

The Bank noted that, during the first ten months of 2024, oil production shrank by 8.5% due to the crisis at the Central Bank of Libya, dropping from 1.17 million barrels per day to 0.54 million barrels per day in September. After the crisis, production rebounded to 1.3 million barrels per day by the end of October, while oil prices remained around $80 per barrel, at the same level as 2023, amidst reduced global demand, particularly from China, and increasing regional geopolitical risks.

The report also discusses the economic trends in Libya over the past decade, highlighting the severe impacts of ongoing instability. The losses are estimated at about $600 billion over ten years, based on the 2015 fixed dollar rate. Had it not been for the conflict, Libya’s GDP in 2023 would have been 74% higher. In addition to instability, key challenges include heavy reliance on oil, lack of diversification, low productivity, and the deterioration of health and education quality.

Ahmad Mustafa, Director of the Maghreb and Malta Region at the World Bank, said Libya faces the challenge of diversifying its economy and reducing its dependence on hydrocarbons. Stability and improved governance will be key to Libya’s economic recovery, as evidenced by the significant economic losses caused by instability in recent years.

Furthermore, by addressing the risks posed by climate events, Libya can protect its infrastructure, ensure the delivery of services, and maintain financial stability, paving the way for a resilient and prosperous future.

The World Bank emphasized that Libya’s economic outlook is heavily reliant on the oil and gas sector, which dominates GDP, government revenues, and exports. Oil production is expected to recover to 1.2 million barrels per day in 2025 and 1.3 million barrels per day in 2026, boosting GDP growth to 9.6% in 2025 and 8.4% in 2026. Non-oil GDP growth is expected to be 1.8% by the end of 2024, driven by consumption, averaging around 9% during 2025-2026. Despite lower oil revenues in 2024, fiscal and external balances are expected to show surpluses of 1.7% and 4.1% of GDP, respectively, due to reduced spending and imports.

The Bank further noted that the country’s priorities include strengthening security, governance, and stability. With GDP per capita reaching $7,570 in 2023, Libya is considered a high-middle-income country. By prioritizing non-oil sectors and encouraging private-sector-led growth, Libya can unlock high-value employment opportunities and enhance development indicators, thus improving the lives of citizens and aligning with the global shift toward clean energy, according to the World Bank.

Libyan businessman Husni Bey stated exclusively to our source: “What is being circulated about the Central Bank’s request to the Audit Bureau is nothing more than a ‘storm in a teacup.'”

He continued: “The Federal Reserve has not suspended any transactions related to Libya, nor has it threatened any immediate or urgent suspension. All it requires is an independent auditing office to conduct post-transaction reviews and monitor the use of Libya’s dollars by Libyan banks and the Central Bank in terms of transparency and combating money laundering and illicit activities.”

Bey added: “The requested measure is merely formal, natural, and objective—especially in a country like Libya, where the parallel market, speculation, and trade outside the banking system through personal cards and cash account for approximately 50% of the economic activity.”

He explained: “The U.S. Federal Reserve’s concerns stem from institutional division, deficit spending, the absence of an approved budget, and the lack of consensus on financial arrangements. This is compounded by allegations of undisclosed public funding sources, oil-for-fuel barter agreements, fuel smuggling, and other irregularities highlighted in the Audit Bureau’s reports. Fuel smuggling, which has become a contentious activity due to price disparities exceeding 3,000%, exacerbates these issues.”

Bey concluded: “We must admit that the fault lies with us. We need to work on unifying the budget or agreeing on financial arrangements, while also taking decisions to limit cash transactions—even criminalizing cash dealings above a certain amount, such as 50,000 dinars.”

He wrapped up his remarks by reiterating: “It is a storm in a teacup, and the Central Bank, through its correspondence with the Audit Bureau, is trying to comply with the request and reduce concerns and risks.”

Mrajaa Ghaith, former board member of the Central Bank of Libya, clarified in his statement to our source regarding the open letter signed by several experts about the financial challenges facing the Libyan state. He stated that the paper is mainly related to the preparation and implementation of the 2025 budget. Its purpose is to encourage the parties involved to agree on a budget that will serve as the basis for spending in the coming year, along with measures to reduce waste, unnecessary spending, and to encourage the collection of the state’s rightful revenues. However, it does not address the overall issues of the Libyan economy, but rather focuses on the 2025 budget with some additional proposals.

Ghaith also stated: “The success of the recommendations depends on the seriousness of the parties in control of the state, and whether they have the will to combat waste and excessive spending without adhering to laws and spending through an approved budget, or whether spending will continue based on personal interests and desires.”

Our source from the Central Bank of Libya revealed in an exclusive statement: “We reassure citizens and traders regarding the correspondence directed to the Audit Bureau about the Federal Reserve. There is no cause for concern, as these are routine administrative procedures that can be managed.”

The source continued: “The correspondence does not pose a significant risk as long as the Central Bank’s management is collaborating with the Audit Bureau to select a review company if necessary, as a precautionary policy.”

He added: “The correspondence includes routine procedures, and the Central Bank continues its foreign exchange sales as usual. We also caution against speculative trading.”

The source concluded: “The issue is temporary and will not affect the availability of foreign exchange in the coming months, as much as it focuses on maintaining relationships with international correspondents.”

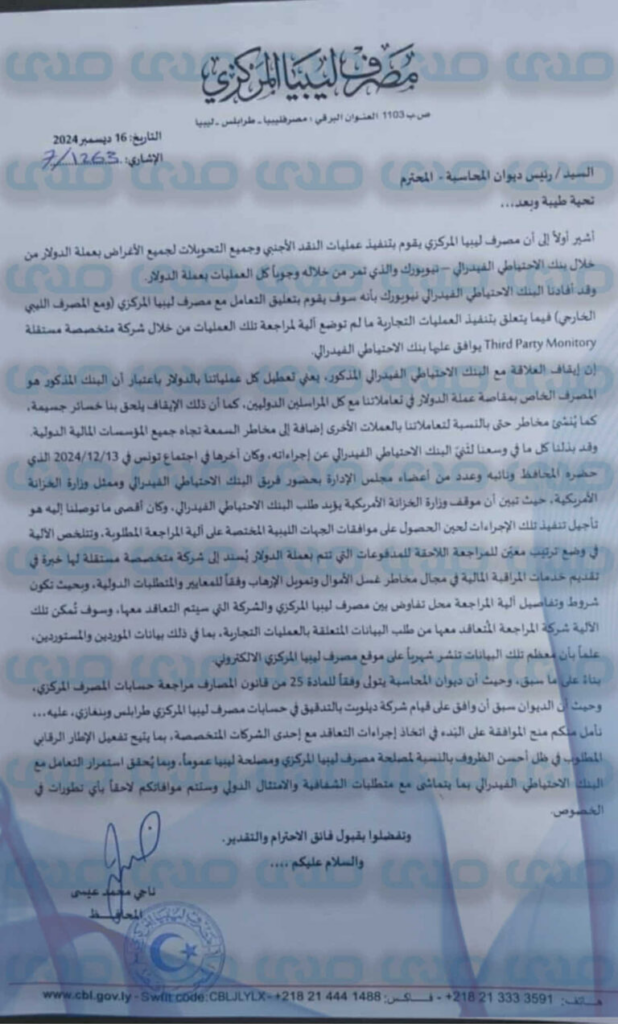

Our source has exclusively obtained a correspondence from the Governor of the Central Bank of Libya to the President of the Audit Bureau. In this letter, the Governor indicated that the Central Bank of Libya executes foreign exchange transactions and all transfers in US dollars through the Federal Reserve Bank in New York, which is the mandatory intermediary for all dollar-denominated transactions.

The Governor stated that the Federal Reserve Bank of New York has informed the Central Bank of Libya that it will suspend its dealings with the Central Bank of Libya (and the Libyan Foreign Bank) concerning the execution of commercial operations unless a mechanism for reviewing such transactions through an independent specialized company, referred to as a Third-Party Monitor, is established and approved by the Federal Reserve Bank.

He further explained that severing ties with the Federal Reserve would mean the suspension of all dollar transactions, as the Federal Reserve is the clearinghouse for dollar transactions with all international correspondents. Such suspension would lead to significant financial losses and expose the Bank to risks regarding transactions in other currencies, as well as reputational damage with international financial institutions.

The Governor emphasized that every effort had been made to dissuade the Federal Reserve from taking this action, most recently during a meeting in Tunis on December 13, 2024. The meeting was attended by the Governor, his deputy, and several board members, along with the Federal Reserve team and a representative from the U.S. Treasury Department. During the meeting, it was made clear that the U.S. Treasury supported the Federal Reserve’s demand. The best outcome achieved was a delay in implementing the suspension until the Libyan authorities approved the required review mechanism.

The proposed mechanism involves establishing a specific arrangement for post-payment reviews of dollar transactions. This would be entrusted to an independent specialized company with expertise in providing financial monitoring services, particularly in the areas of anti-money laundering and counter-terrorism financing, in accordance with international standards. The terms and details of this review mechanism would be subject to negotiations between the Central Bank of Libya and the selected company. This mechanism would grant the contracted auditing firm access to data related to commercial transactions, including supplier and importer information. It is worth noting that most of this data is already published monthly on the Central Bank’s website.

In conclusion, the Governor stated that, based on the above and in light of Article 25 of the Banking Law, which entrusts the Audit Bureau with auditing the Central Bank’s accounts, and considering that the Bureau had previously approved Deloitte’s auditing of the Central Bank’s accounts in Tripoli and Benghazi, he requested approval to proceed with contracting one of the specialized companies. This would enable the implementation of the required regulatory framework under optimal conditions for the benefit of the Central Bank and Libya as a whole. It would also ensure continued engagement with the Federal Reserve in line with transparency and international compliance requirements. The Governor pledged to update the Audit Bureau on any further developments in this matter.

Esam Hamza, the Director of the General Manager’s Office at Al-Yaqeen Bank, announced that the bank is operating smoothly and at an accelerated pace in the final quarter of 2024.

Mr. Hamza emphasized that all products and services were fully reinstated in October, in line with the directives and circulars from the Central Bank of Libya. He highlighted that the bank continues to offer high-quality electronic services designed to save time and effort for both individual and corporate customers.

Looking ahead, Hamza noted that 2025 will be a landmark year for the bank, as it prepares to roll out a new range of advanced electronic services and self-service machines. These innovations will enable customers to access most services without the need for paperwork or direct assistance from bank staff.

The financial and economic expert, Sameh Al-Kanouni, spoke exclusively to our source about correspondence among experts regarding Libya’s public financial challenges. He stated, “This is entirely accurate and 100% true.”

He added: “I am not pessimistic, but when I see several global oil companies changing their names to energy companies, it raises concerns about the future of oil. These companies are shifting to renewable energy, such as wind and solar power. In 20 years, oil might become marginal, with limited demand confined to industries using heavy oil. Meanwhile, electric cars, phones, and Tesla products, for instance, are powered by renewable energy sources like solar.”

He continued: “We must reduce spending and shift toward investment. I hope recommendations and plans are included when discussing these issues. When addressing a challenge, alternatives should be presented. One key step is encouraging the Investment Authority, reforming the investment law, and transforming it into a Ministry of Promotion and Investment, granting it the authority and strength to attract investors to Libya.”

Al-Kanouni also highlighted the need to revise and update some economic laws to align with the country’s current situation, amend certain Central Bank of Libya regulations, and establish sovereign and investment funds to promote domestic investment. He called for the activation of the stock market and support for local industries in Libya.

He further stated: “Libya’s deteriorating economic conditions are shared by other nations, such as Tunisia, Italy, Turkey, and Egypt.”

He concluded: “I wish these recommendations had been issued years ago. However, it was a courageous step by the meeting participants to convene and provide indicators to decision-makers across all sectors. They proposed measures for spending control and standards. The state must prioritize essential goods for citizens and activate the municipal guard to regulate prices and balance the Libyan market.”

A group of economic and financial experts, including ten members from the Economic Salon organization out of seventeen, consisting of: Dr. Abubakr Abu Al-Aid Abulqasim, Mr. Hamuda Al-Aswad, Mr. Mrajea Gaith, Dr. Abdelghani Al-Fatissi, Dr. Fathi Al-Majbari, Eng. Mohamed Khaled Al-Ghweil, Dr. Mohamed Ben Yousef, Dr. Suleiman Al-Shahoumi, Mr. Mohamed Al-Shukri, and Dr. Ezzeddine Ashour, have issued an important message about the Libyan state’s financial challenges, under the sponsorship of the Human Dialogue Center.

Regarding the current economic situation:

Anyone who cares about the Libyan people must speak the whole truth to them. Therefore, speeches of evasion and aligning with the distortions in the economic situation only serve narrow interests and are a gamble with the country and its future generations.

The standard of living has declined over the last decade, with poverty rates increasing and the per capita share of GDP shrinking, alongside a significant rise in actual inflation rates, unemployment, and the erosion of citizens’ savings. The large disparity in economic opportunities between citizens threatens political instability due to the accumulation of feelings of marginalization, whether real or imagined. This becomes even more likely when such feelings are combined with regional and social narratives of marginalization.

The overall financial indicators have reached levels that threaten financial sustainability and undermine efforts toward stability. Therefore, it is necessary to begin a comprehensive program for restructuring the Libyan economy.

Institutional divisions, both horizontal and vertical, have increased the confusion in managing the country’s economic and financial affairs. Regardless of the proposed temporary solutions, they cannot replace the need for unifying administrative and financial decisions by bringing all political institutions together and renewing their legitimacy through general elections.

Regarding the general budget:

The general budget of the state is supposed to reflect a strategic vision and be a tool for financing, oversight, and monitoring. Unfortunately, it is currently only used for current expenditures, which undermines its effectiveness and weakens its political and social credibility.

There is a need for a unified budget covering all government expenditure items across all regions of Libya. Despite all possible reservations, a unified budget remains better than any other financial arrangements.

The budget should be realistic, taking into account expected needs and revenues. It should also be based on macroeconomic and sectoral quantitative and qualitative indicators, ensuring the possibility of monitoring and evaluation within the framework of fiscal policy. The absence of economic indicators in general budgets reflects a regrettable approach to public funds with an exploitative mindset.

Regarding revenues:

All public entities tasked with collecting public revenues must do so. No entity should retain or deduct any part of these revenues for any reason or transfer them to other entities without legal authority.

All proceeds from the sale of oil, gas, and petroleum derivatives, as well as all other sovereign revenues, should be deposited, without exception, and on time into the general revenue account of the Ministry of Finance.

In a country that primarily relies on oil revenues, the National Oil Corporation must disclose detailed monthly data about its exports, the quantity of each type of crude oil, the selling price, the foreign partner’s share, and the share of the public treasury.

Regarding expenditure controls and standards:

The government and the National Oil Corporation must urgently end the practice of bartering oil shipments to meet local market fuel needs. These needs should be accurately determined and supplied according to the required quantities. The National Oil Corporation should contract with global refineries through transparent procedures. Both the National Oil Corporation and the General Electricity Company must conduct monthly reconciliations to determine the actual supply of gas, crude oil, and its derivatives to the company.

For economic and security reasons related to stability in Libya, fuel subsidies should be restructured in accordance with a studied and gradual policy that provides a social safety net and enhances citizens’ purchasing power, while first gaining their trust through communication, transparency, and disclosure.

Rationalizing expenditures on salaries and subsidies may be inherently harsh and painful for some social groups. However, the state must adopt a policy of truth with citizens and stop the practice of appeasing public opinion for the benefit of narrow interests.

In terms of rationalizing expenditures, the following measures should be implemented in the 2025 budget:

Cease government appointments and salary increases throughout 2025 to allow for an accurate census of public employees and identification of actual needs.

Issue a unified salary schedule that considers the cost of living and ensures a reasonable balance between higher and lower grades.

Review the inflation of some budget items, such as subsistence, accommodation, and vehicle purchases.

Reduce the number of government agencies funded by the general budget by merging public institutions with similar goals.

Reduce the number of Libyan embassies and diplomatic missions abroad and their staff.

Cease spending large sums of public money on social issues like marriage without proper economic and field studies showing the impact on the targeted groups.

We urge the relevant authorities to activate and support the following institutions for their vital roles in economic development: the Civil Registry Authority, the Real Estate Registry, the Statistics and Census Authority, the Tax Authority, the Urban Planning Authority, the Public Property Authority, and Customs.

Priority in development should be given to energy, electricity, basic social services, and infrastructure projects. In all cases, financial allocations for targeted projects should include their names, geographic distribution, value, and required cash flows over the execution period.

We emphasize adherence to the rule of not transferring funds from the third section (development) to other sections in the general budget.

Regarding monitoring and evaluating the budget implementation:

The signatories of this message are aware that the general budget includes structural facts that are sometimes difficult to overcome, such as the inflation of public employee numbers, the reliance of many citizens on subsidies, and the widespread corruption in administration. However, they are also aware that addressing these structural distortions and combating corruption takes time and requires determination, planning, and design to avoid turning good intentions into ill-conceived and poorly studied decisions that fuel conflicts.

All public entities should be subject to monitoring by oversight bodies, which enhances transparency and governance.

We emphasize that all public entities issue monthly reports on revenues and expenses, as well as reports on the progress of development projects, their costs, and any increases or savings in funds and time.

The Audit Bureau and the Administrative Control Authority should issue quarterly reports on the expenditure of development allocations, in addition to the annual report in the first half of the following year to address violations before they worsen.

All state institutions must close their final accounts, which allows for determining their financial position and identifying obligations and debts to the public treasury.

Regarding accompanying reform measures:

We urge the legislative and executive institutions and expert houses to review all legislation related to the state’s financial and economic system. These reviews must be conducted in a systematic and consultative manner to ensure their smooth implementation.

Until that happens, institutions must adhere to current legislation in their financial management according to principles of cooperation and professionalism that should prevail between state institutions.

A population census and basic surveys should be conducted to provide sufficient indicators to guide economic decisions and their appropriate timing.

Economic and financial data should be provided and published, enhancing their inclusiveness and reliability.

Resources should be allocated to municipalities, granting them the authority to spend them on their defined development priorities.

Priority in public procurement and contracts should be given to the Libyan private sector.

The public treasury should not bear any financial obligations that are not included in the general budget. The Ministry of Finance should efficiently manage the state’s assets from public companies and sovereign funds, maximizing their revenues and ensuring they are not diverted outside the general budget.

Procedural steps for adopting the budget:

If the economic situation is exceptional, the upcoming year’s budget should also be dealt with exceptionally to ensure its adoption, compliance, and smooth implementation. This requires wide political agreements among the key parties and active communication between technical bodies and the relevant political institutions.

The Central Bank of Libya must maintain its independence and work within its legally defined responsibilities to ensure its professionalism and neutrality. The relationship with the Ministries of Finance and Economy should be arranged so that each can implement its powers without overlap.

In conclusion, dealing with economic challenges seriously and responsibly requires launching a comprehensive political process that integrates its various paths without delay or postponement from the UN mission. If Libya needs a solid national charter between its political and social components, it also requires a deep dialogue about the desired economic model that should guide the work of all institutions and address the root causes of repeated conflicts.

Our source has obtained a notice referred by the Deputy Director of the Audit Bureau, Atiyat-Allah Abdulkareem, to the Bureau’s Legal Affairs Office. The notice was received by a process server from an unidentified citizen, who claims that Khaled Shakshak is no longer the Head of the Audit Bureau. The citizen bases this claim on rulings issued by the Tripoli Court of Appeals.

In response, the Legal Affairs Office stated that this notice holds no value and has no basis in reality or law, noting that the rulings mentioned had been overturned and annulled by the Supreme Court.

The Bureau’s Legal Affairs Office confirmed that the legitimacy of its head is derived from rulings by the Constitutional and Administrative Divisions of the Supreme Court, as well as decisions from both the House of Representatives and the State Council, which extended his term as head of the Bureau according to the provisions of the Political Agreement.